Credit card debt is one of the leading causes of financial hardship and is a budget killer.

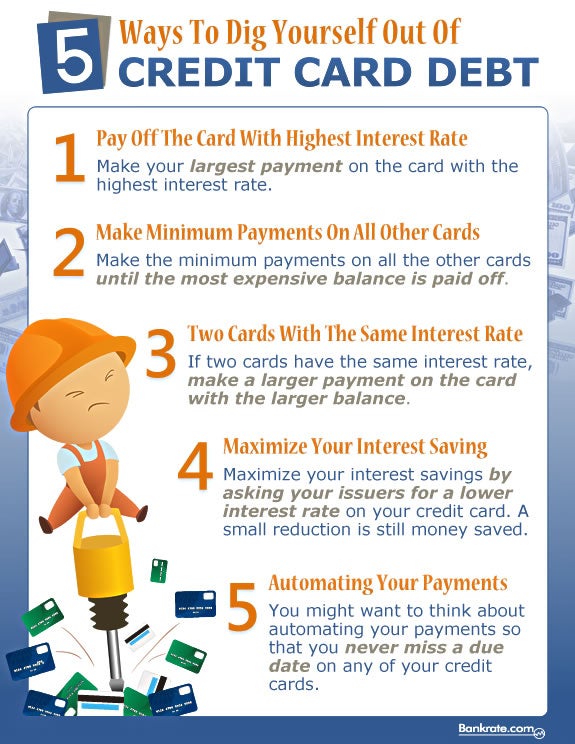

Here is cool infographic by Bankrate.com for 5 ways to dig yourself out of credit card debt.

Share your tips below.

Source: Bankrate.com

Credit card debt is one of the leading causes of financial hardship and is a budget killer.

Here is cool infographic by Bankrate.com for 5 ways to dig yourself out of credit card debt.

Share your tips below.

Source: Bankrate.com

Published September 14, 2014

Many of my private clients who were dealing with money or credit woes were also dealing with major depression as a result of their financial situation. Whether their challenging financial situation was due to a job loss, excessive debt, unexpected financial expense, or lack of money management skills and knowledge; the emotional stress then caused significant mental and physical illnesses like high blood pressure, anxiety attacks, etc.

Many of my private clients who were dealing with money or credit woes were also dealing with major depression as a result of their financial situation. Whether their challenging financial situation was due to a job loss, excessive debt, unexpected financial expense, or lack of money management skills and knowledge; the emotional stress then caused significant mental and physical illnesses like high blood pressure, anxiety attacks, etc.

I can absolutely relate. So now I am sharing my Financial Depression Confession. I am sharing how my money woes made me feel like it was the end of the world and what I did to help myself get better. My hope is that my transparency with this experience will help someone get through their extremely sensitive and painful period of financial depression.

I dealt with major depression. I didn’t want to get out of bed, wasn’t motivated to clean my house, didn’t want to talk or see anyone, and I cried … A LOT! I suffered from insomnia and exhaustion. I over ate and didn’t exercise, so of course I gained lots of weight, which killed my self-esteem. This vicious cycle made me feel like it was the end of the world! I even contemplated suicide, but honestly … I couldn’t even “financially” afford to kill myself. Wait! Before you judge … depression is a severe psychological illness and if not treated, it can cause the sanest person to consider or do insane things.

WHAT I DID: I got help! I went to a clinical counselor to talk about my feelings. I know what you may be thinking, but talking out some major emotional insecurities and feelings with a qualified third party helped me to deal with those emotions. It also gave me an unbiased support system. I was reminded that my emotions were normal, which helped me to realize that what I was going through was NOT the end of the world. By purging my private pain, I was able to free my mind to think more logically.

Emotionally and mentally, I was paralyzed. I just couldn’t move past what I was going through. Yes, I prayed and did my best to trust that God would get me through it, but I just couldn’t do what was necessary to allow God to move. “Faith without Works is dead!” I knew that Bible verse and said it to myself every day. But … I felt helpless and hopeless which kept me paralyzed.

WHAT I DID: I changed my MIND! I realized that the eyes may be the strongest muscles in the body, but the Mind (brain) is the hardest muscle to change. So, I worked at it everyday. I changed what I watched, read and listened to. I became extremely protective about what I allowed to enter my mind because Thoughts turn into Words, Words turn into more Thoughts and those Thoughts turn into Actions or Non-Actions. What we visualize will actualize (positive or negative) so I only allowed positive and actionable thoughts, through affirmations, songs, books, etc.

I didn’t believe that anyone would understand what I was going through. I’m Madam Money! How could anyone understand “how” or “why” I was dealing with Money Woes? I didn’t think that anyone would understand, so I isolated myself. It was a very lonely place to not have anyone I could trust to share that I was dealing with my deepest and darkest fears of about money.

WHAT I DID: Once I realized that this “lie” I was telling myself was bred from my PRIDE. I was too proud to ask for help. So, I had to humble myself and ask my a core circle of family and friends for help. I established specific roles for each of them to help me. For example, I had friends that helped me and held me accountable for eating better and exercising, friends that made me get out of the house to avoid isolation, and a family member that helped me financially when I absolutely needed. Asking for help was the hardest thing for me to do, but it was the best thing I could have ever done. And guess what, they understood because they had experienced what I was going through.

I medicated my pain through spending money on eating out every day, drinking and shopping. Oh yes I did! Dealing with the pain was too painful. So I tried to numb the pain by doing the opposite of was I know to do. Knowing what to do and how to do it but doing the opposite is “self-sabotage.” I become my own worst enemy. I became my most challenging client.

WHAT I DID: I got help from another financial coach. Yup! Coaches need coaching too. Even though I didn’t need my coach to tell me what to do; I needed my coach to hold me accountable to do what I know I’m supposed to do. My coach guided me through the process as a support system to stop my financial hemorrhaging caused by my financial self-sabotage.

Everything I did to try to improve my situation, just didn’t work. The more my attempts failed the more I doubted myself and my ability to fix my situation. How do you destroy the most confident person in the world … DOUBT! Doubt is the direct result of Fear, which is “False Evidence Appearing Real.” Bottom line … I was afraid to fail and because my attempts weren’t working, this failure made me doubt everything.

WHAT I DID: Believe it or not … I connected with others! By connecting and networking with other people and professionals, I had intellectually stimulating conversations. Those conversations helped me build new relationships and networks. Those new relationships and networks valued my connection because of my personality, expertise or passion. This built up my confidence. Not only that, I connected with people who experienced my challenges, or knew someone who could assist me with my some of my challenges. This built up my confidence and reduced my doubt.

I’m not saying that everything that I did to help me will help you. But I am saying that there is HOPE and HELP for anything that you may be going through.

Whatever you are going through, even though it may feel like it … it is NOT the end of the world. It is the beginning of a new opportunity to make you stronger than ever to improve your current financial situation.

If you are experiencing financial depression and need help, I am here for you. I look forward to being a resource to help you through my pain, passion and purpose.

by Lexington Law

In much the same way that a resume displays your work experience to a prospective employer, a credit report provides prospective creditors (and in some cases employers and insurers too) with a detailed picture of your credit history. And like a resume, your credit report can influence whether you will receive what you are applying for.

Ideally, your credit report is an accurate, up-to-date reflection of your credit history. However, since we don’t live in an ideal world, there are many reasons that your credit report could contain inaccuracies that might prevent you from receiving the credit you deserve. The good news is you can take action to keep your report accurate. Here are the top five reasons why you should make a practice of regularly reviewing your credit report:

Inaccuracies & Mixed Credit Files

Inaccuracies & Mixed Credit FilesMany inaccuracies on a credit report can be the result of simple human error, and are therefore are not difficult to dispute. Of course, if you don’t order your credit report, you might never know about it. Whether the inaccuracies relate to payments not credited, late payments, or data mixed in from the credit file of someone else with a name similar to yours, you will want to contact the credit bureau to dispute inaccurate information promptly.

One of the most important elements of credit is a demonstrated history of on time payments. Once you send the check though, anything can happen–a delay in the payment being received can kick you over to a 30-day delinquency. If you call your creditor and explain the situation, they might adjust the information. Of course, if you don’t read your credit report, you won’t necessarily know which payments are being received and reported properly.

This issue alone is reason to order your credit report immediately. Identity theft is an insidious crime, involving a thief who assumes your name to open new accounts, divert your card statements to another address, and run up all sorts of bad debt without you ever knowing about it until collectors come calling. Over time, identity theft could jeopardize your ability to obtain further credit. The best way to catch a thief who is using your name is by getting a copy of your credit report, which will show you if there are accounts listed you know you haven’t opened. For example, if a thief has intercepted a pre-approved credit card offer in your name and sent it in with a change of address, your credit report will include the account.

If you’re shopping around for a loan or more credit, you should know that when creditors check your credit, it places an inquiry on your credit report. Inquiries can add up, which is often interpreted as a negative by creditors. For this reason, too many inquiries can actually make getting credit more difficult. Moreover, if you didn’t authorize

someone to look at your credit report and they did, they may have broken the law.

Credit fraud involves the theft of your credit card or account number to make unauthorized charges to your account. Though consumers are protected financially from this abuse, other creditors may take note of all this activity and decide to raise your interest rates or refuse to grant you a loan. Ordering your credit report will help you catch new activity on accounts that you haven’t been using, or may have closed.

When it comes to managing your credit worthiness, your credit report is your best resource. Ordering your credit report gives you the opportunity to manage your credit wisely today, while planning your credit strategy for achieving future goals–a credit-savvy move every consumer should make!

Financial Freedom, like salvation, is available for EVERYONE. However, even though we have access to it, there are principles or “commandments” that should be obeyed. So, here are the “10 Commandments for Financial Freedom.”

Diets are meant to be temporary; and if you can’t sustain it, old behaviors may return. Make positive financial changes that can be easy to incorporate in your “Lifestyle” and can be maintained over time to improve and enhance your financial situation.

Get all of your financial statements and bills organized. This will be helpful when building and updating your spending plan (aka a budget).

Every little bit counts with building savings. Start with a small savings goal and build up over time.

Saving is the key. Not only for emergencies but for opportunities and your future. Make sure you put your oxygen mask on first financially to ensure you have enough to help yourself and your family.

Before deciding to make a large purchase, give yourself a few days to think about the purchase or find a cheaper price. Buyer’s remorse is a pain in the …. (you know what)!

Structuring when your bill payments are due will help you comply and regulate your spending plan (aka budget). Paying your credit accounts will help improve you credit reports because payment history is 35% of credit scores.

Use cash as much as possible! This will help you take control of compulsive spending and avoid adding on to existing debt.

Feeling deprived leads to splurging. So, don’t focus on what you can’t do or spend. Rather, focus on what you will be able to do and spend when you plan and budget for it.

Do something small and frequent to treat yourself for keeping up with your spending plan (aka budget) and the goals you set for yourself. Moderation is key, so make sure you Reward Yourself Responsibly.

One of life’s greatest pleasures is to be content with what you have. It is good to desire more to drive you towards your goals and plans, but being content makes the journey more pleasurable.

Comply with these commandments and enjoy the Financial Freedom you desire and deserve!

Syndicated | Tayne Law Group

Are you in Financial Denial? If the answer is NO, then you probably are. Just kidding. However, Jimmy Ingrilli, from the Tayne Law Group Blog, shares 5 signs you may be in Financial Denial.

While the reasons may differ from person to person, one answer can be their willingness to correct money problems if and as they arise. A hallmark of being financially responsible is taking action to right your money ship, while someone in financial denial is not able to admit they are having financial problems. It can be hard to admit or even notice a money problem exists, so here are some signs you may be in financial denial.

If you’re dishonest, look to avoid conversation, or even downplay financial issues, then there’s a good chance you are in financial denial. Avoiding financial problems will not only hurt you, but can also hurt your loved ones. Financial dishonesty can lead to further disaster as your family members may spend money based on how they believe they stand financially. Someone who is financially responsible should know their income, exact debt, credit score, what their budget is, how much they should save, and have long and short term financial goals.

While borrowing money may seem necessary at times, a person living in financial denial believes borrowing money is the norm. They may rely heavily on credit cards or borrow from friends and family in order to pay off debt and bills. In other words, they “rob Peter to pay Paul.” This will never get you on track as you are only taking on debt to pay other debts and will never teach you responsible financial habits.

These days, debt is a household word and is often used to help us purchase big-ticket items. Good debt can be any loan you take on with the ability to pay back or any debt that can generate future income such as a school loan, … (continue reading Signs you’re in Financial Denial)

Are you (or someone you know) recently divorced? I’m not … but I’ve worked with several clients who are.

If are recently divorced, you may be feeling not just the loss of a partner, but also the absence of the second paycheck. Chances are, you have been living a lifestyle based on two incomes, and now that you are the sole provider there are some changes that will need to be made. First important thing is to determine what you can live on by compiling your household and other bills and adding them up, including your food and gas expenses. Then try these 5 Quick Financial Survival Tips for the Recently Divorced.

Downsize Housing or Seek Assistance

If your rent is more than you can handle, you can search for a smaller more affordable apartment. Or if you can’t afford your mortgage alone, you can try to refinance or put the home on the market for sale. Consult with a real estate professional to help you through the process in the event a Short Sale is necessary. There are also nonprofit organizations that provide assistance with foreclosure prevention.

Reduce Cable & Cell Phone Bills

There are some quick things you can do to help you through the first year, such as reducing your cable and cell phone bills. Many of us have more channels than we watch, and now would be a good time to check to see what you are paying for and remove any channels or extra cable boxes that you do not need. Change your cell phone plan to basic usage, if possible. However, if your cell phone is your primary telephone, have your cell phone usages evaluated to find a better or more affordable plan. Also, removing any extra features and also choosing a plan with fewer minutes. Cancel your landline telephone service, if it is rarely used.

Shop Smaller Portions

Shopping for groceries may take some getting used to, especially if you have been in a relationship for a long time. You may want to buy smaller packages of things such as meat, or freeze the portion that you will not use immediately. Make a list and use coupons. Eating at home and bringing your lunch to work will reduce those extra expenses.

Increase Your Income

If you find that after doing everything humanly possible you still do not have enough to live on, then you may want to take on a part-time job to offset your expenses. This may be a challenge, especially if you have children. So, consider starting your own home based business or connecting with a network marketing organization that is right for you with a good compensation plan and reasonable independent business owner investment.

Update Your Beneficiaries & Tax Withholding

One of the most common things that recently divorced people neglect to do is update their beneficiaries on their insurance policies, bank and investment accounts. Make sure you update all financial documents that have or require a beneficiary. Also, don’t forget to update your tax withholding on your W-4 or W-9, if necessary. Consult with your personal financial team to make these changes completely and correctly. If you don’t have your own personal Financial Team, create one that consists of your favorite Banker, Insurance Agent, Investment Adviser, Tax Accountant and Financial Coach, like me, to help you through this process.

Changing your lifestyle is hard enough without having to go through a divorce. Now that it is just you, and your children if you have any, altering your budget and spending habits will help you sustain your lifestyle. Cutting back where possible and necessary will give you greater flexibility with your spending plan or budget.

[us_separator type=”default” icon=”fas|dollar-sign”]What are some additional Financial Survival Tips for the Recently Divorced?

© 2026 Madam Money®. All Rights Reserved. | Designed by SRJWebsites.com

You must be logged in to post a comment.