Black Enterprise Sr, VP & Editor-at-large and host of The Urban Business Roundtable, Alfred Edmond, Jr interviews Madam Money on his new podcast "Money Matters." Listen to how to Guard…

Read More

By now I’m sure you have heard or read about Equifax’s massive security breach that exposed personal and financial information for over 140 million consumers.

I know what you’re thinking …

“What’s the Equifax Data Breach got to do with me?”

Well, not only were credit card and other credit account numbers acquired by the hackers … social security numbers, addresses and birth dates among other sensitive personal information were stolen. Your personal information may be among the 140+ Million consumers.

“WTW (What The Wealth) do I do now?”

I’m glad you asked. Here are 5 quick things to do right now.

Equifax has created a new website for consumers to check if they have been impacted. Go to https://www.equifaxsecurity2017.com/potential-impact/ to find out if you are one of the ones impacted today.

If you are one of the (un)lucky ones impacted … hold up, wait a minute! Before you enroll in their program, read the fine print to make sure you don’t waive your right to sue them in the future. Look for the “Arbitration Clause.”

You are entitled to at least 1 (some states may allow up to 2) #Free copy of your Credit Report from all three Credit Reporting Companies (Equifax, Experian and TransUnion) annually. You can also get a free copy of your credit report when you have been denied credit based on information in your credit report.

Go to http://www.annualcreditreport.com to get a free copy of your credit reports today.

Don’t worry! It’s easy and the website walks you through what to do.

Each Credit Reporting Company (Equifax.com, Experian.com & TransUnion.com) has a service to Freeze your credit report so no one can access your information. They may charge a small fee to do it, but it just might be worth the investment.

Just remember to UnFreeze your credit report(s) before you apply for Credit.

Get your Credit Score for #Free from Credit Sesame at https://tinyurl.com/ydgf4rkg. Just keep in mind that the credit score you will see is considered an “Educational Score” and will be different than the credit scores pulled and viewed by Financial Institutions.

Related: The Truth About Credit Scores for Consumers

Credit Sesame also has Identity Theft Insurance as well as a Credit Monitoring program.

Stay abreast of what is going on with this data security breach, as well as money tips and ways to protect and Cover Your A$$ets at https://www.madammoney.com. You can also send your questions to info@madammoney.com.

[ctt template=”8″ link=”cbtba” via=”no” ]Knowing what is on your Credit Report will make it easier for you to identify changes and take the necessary action immediately.[/ctt]

Post your tips below and don’t forget to #Share this info with everyone you know. ![]()

![]() ❤

❤

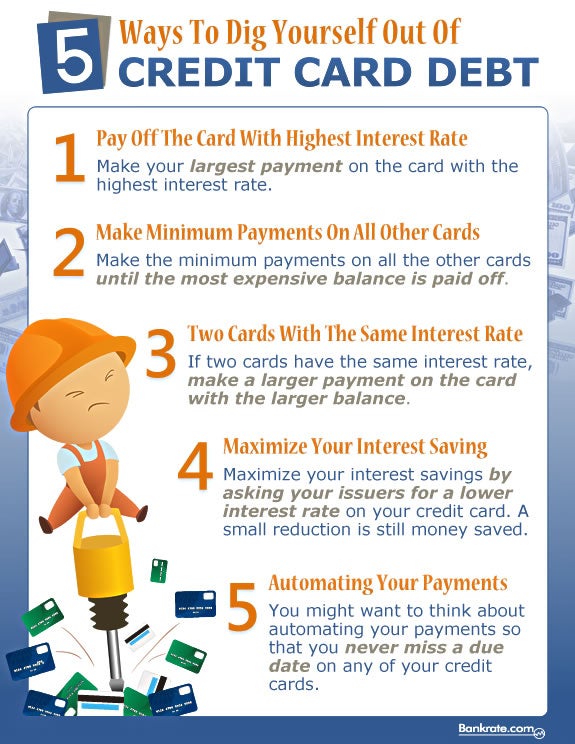

Credit card debt is one of the leading causes of financial hardship and is a budget killer.

Here is cool infographic by Bankrate.com for 5 ways to dig yourself out of credit card debt.

Share your tips below.

Source: Bankrate.com

Many consumers are in financially abusive relationships with banks that are “not that into” them. These consumers are dealing with ridiculously high loan interest rates, very low deposit rates, too many and extremely high fees, as well as poor customer service.

When I was in a financially abusive relationship, it not only angered me, it made me feel weak and hopeless because I didn’t know how or if I could escape. Then one day … I did! I left my “un-wealthy” financially abusive relationship with my bank.

Here are three effective Exit Strategies for getting out of a Financially Abusive Relationship from my book, Financial Fornication.

The opportunity of improving your financial situation happens by talking with the right person at the bank. So, before deciding to break up with your bank, be sure to …

If efforts to resolve the matter are not addressed appropriately or ignored, move to the next strategy.

Begin the process of financially dating other financial institutions to find one (or two) that meet most of your required financial needs (deposit accounts, loans, internet banking, etc.). In my book Financial Fornication, I share in detail the 5 phases of Financial Dating to avoid getting into financially abusive relationships.

These phases should not be skipped. It is necessary and worth taking the time to get to know financial institutions to make sure they are right for your personal or business financial situation.

Once your new financial “main squeeze” is found, it will make it easier to leave your existing bank.

Whether a new financial “main squeeze” is on standby or not, slowly stop using the bank’s products and services.

Be sure to…

Once these steps are executed, a clean break is relatively easy.

Even though the financial relationship may seem extremely challenging right now, just know that all financial institutions are not the same. There are lots of really good banks and credit unions out there that value and appreciate their customers. Once you find them, some of them even provide an easier method of transiting automatic payments and direct deposits to them through what is called Switch Kits.

So don’t give up. There is hope. And most importantly, you deserve better!

For more tips on how to have a more wealthy relationship with your money, read my book, Financial Fornication on Kindle or Amazon.com.

Saving and investing — they’re both critical to achieving your financial goals. They both require you to put money aside, but for very different purposes.

Saving is ideal for short term goals (vacations or a rainy day fund). Investing is for long-term goals (down payment on a house or retirement).

But if you’re confused by the difference, you’re not alone. Most people in the U.S. don’t save enough, according to think tank Economic Policy Institute. And only half invest, according to a recent report from polling organization Gallup.

Take a look at this video. It will help you understand the difference between saving and investing.

Originally appeared on Learn.Stash.com and written by Jeremy Quittner, the Stash financial writer.

© 2026 Madam Money®. All Rights Reserved. | Designed by SRJWebsites.com

You must be logged in to post a comment.